Business Owner Alert: Paycheck Protection Program

Published Thursday, April 1, 2020, 4 p.m. EST

— A cornerstone of the U.S. Government response to the economic crisis caused by the pandemic is the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), a history-making $2.2 trillion law that just went into effect. With almost no strings attached, CARES extends financial support to business owners in need under the Paycheck Protection Program (PPP).

PPP is a safety net for businesses with fewer than 500 employees — mom and pop shops, restaurants, professional services and other small businesses that created 70% of the new jobs in the U.S. in the past decade — the vast majority of which have 10 employees or less. Self-employed and contract employees also qualify for PPP.

PPP provides small businesses with funds to pay up to eight weeks of payroll costs including:

- Salary and wages

- Commissions

- Tips

- Paid leave

- Health insurance and healthcare payments

- Retirement benefit payments

- Some independent contractors

Funds can also be used to pay interest on mortgages, rent, and utilities. To be clear, as long as you use the loan proceeds to pay for qualified expenses within eight weeks, the loan is forgiven.

- Funds are provided in a loan that may be fully forgiven if used for payroll costs, interest on mortgages, rent, and utilities.

- At least 75% of the forgiven amount must have been used for payroll.

- Loan payments will also be deferred for six months.

- No collateral or personal guarantees are required.

- The government will pay the origination and other costs for administering these loans.

The maximum PPP loan you are eligible to receive is 2.5 times your average monthly payroll for the past 12 months for the eight-week period, subject to these key limitations:

1. If you pay more than $100,000 a year to an employee, the excess over $100,000 does count toward the maximum you loan you qualify to receive.

2. The maximum loan a company is $10 million.

For example, if you paid 10 employees $1 million for the past 12 months, then your average monthly payroll for the period was $83,333. Your maximum loan would be 2.5 times the $83,333 in monthly payroll, or $208,333.

The loan will be forgiven, but you must use the proceeds to pay these qualified expenses within eight weeks:

- Payroll

- Group health care benefits

- Salaries

- Mortgage

- Rent

- Utilities

The loan amount that is forgiven will not be subject to tax and you also can deduct it as an expense, putting even more power behind the PPP benefit.

PPP Compliance Caveats.

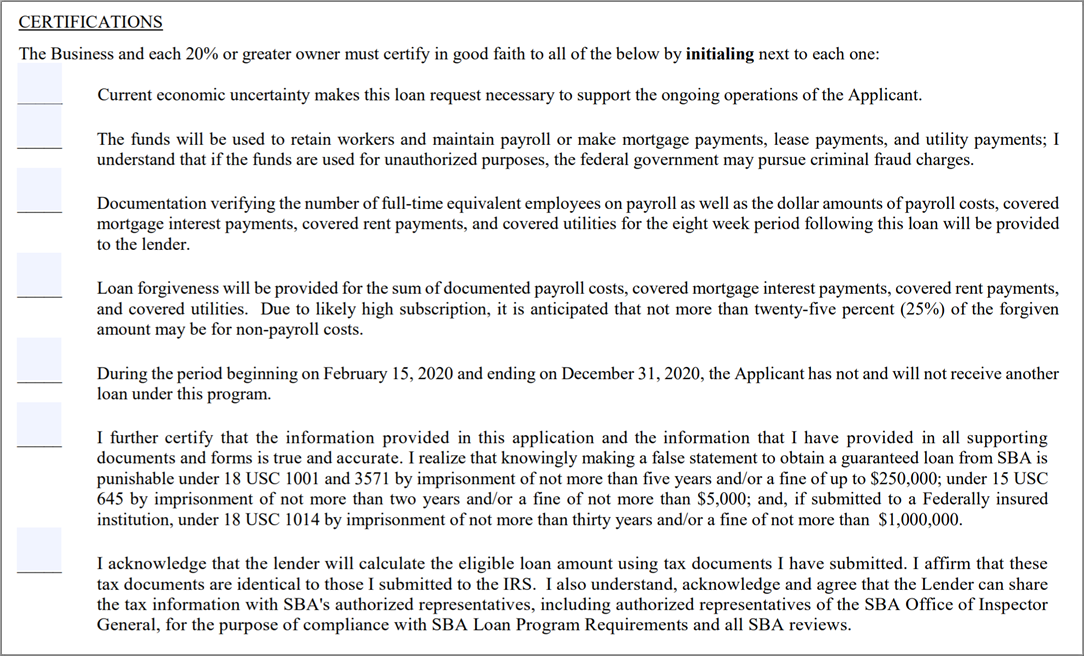

You must certify with your signature a "good faith certification" saying the loan is necessary to support the ongoing operation of your business and will be used to retain workers, make payroll, mortgage, lease and utility expenses. If you have six months of cash on hand, for example, you may not be able to certify the funds are necessary. However, some businesses may operate at a higher profit as a result of PPP relief and may still qualify for the loan forgiveness program. If you have questions about whether you can certify in good faith that the PPP funds are necessary to the ongoing operation of your business, it’s wise to consult with a qualified professional.

The intent of the law is to enable your business to continue to pay employees, including contractors, through the partial shutdown of the economy from February 15, 2020 through June 30, 2020. If you reduce your payroll, your loan amount will not be fully forgiven. Calculating how much of your loan would be forgiven after reducing your payroll requires personal, decisions about personnel and calculations by a professional.

To comply with PPP rules, you may want to segregate the loan proceeds in a separate account that your company will tap only to pay for qualified expenses.

This article does not address financial economic consequences of the Act for investors but summarizes what business owners need to know about the financial lifeline coming.

Nothing contained herein is to be considered a solicitation or research material. It is subject to change without notice. Strategies referenced herein do not take into account your personal objectives, financial situation or particular needs of any specific person. The material represents an assessment of financial, economic and tax law at a specific point in time. The sources are thought to be reliable but could be wrong about important facts.

The U.S. Government's response to the Coronavirus crisis implements new regulations and their precise impact may not be available at the time this was written or could be subject to change by U.S. Government agencies, such as the SBA..

© 2024 Advisor Products Inc. All Rights Reserved.